Functional expense reporting became a requirement a few years ago when nonprofits implemented Accounting Standard Update (ASU) 2016-14, Not-for-Profit Entities (Topic 958): Presentation of Financial Statement of Not-for-Profit Entities. Have you given much thought since then to what you’re reporting? We’ve summarized some key points about functional expense reporting and some things to consider as you approach year end.

What is Functional Expense Reporting?

The purpose of reporting expenses on a functional basis is to provide the users of your financials (i.e. your Board, members, management) an overview of the Association’s use of resources to carry out their mission.

How is it Presented?

Most commonly, the analysis of functional expenses is presented in a separate statement called “Statement of Functional Expenses.” Alternatively, the analysis could be presented within the Statement of Activities or in a footnote disclosure.

The analysis of functional expenses shows the expenses of an association in natural categories (salaries, travel, rent, printing, food & beverages, etc.) and how these are incurred across each functional area of the association. Associations should consider the users of their financials when determining how detailed these natural categories should be.

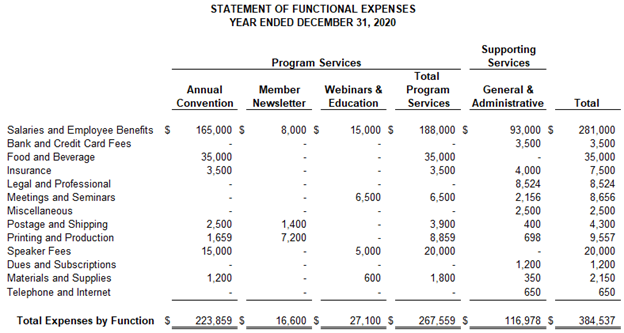

Functional areas are divided into two main categories: program services and supporting services. If useful to the financial statement users, program services can be further classified into specific programs or services that the association provides, such as annual meetings or conventions, member services, publications produced, etc. Below is an example of a Statement of Functional Expense.

Why is Functional Expense Reporting Important?

Many associations are granted tax exempt status by the IRS under Section 501(c)(6), Business Leagues and Trade/Professional Associations. An association under this section exists to promote a common interest, trade or profession and is largely supported by their membership.

The true purpose of the functional expense analysis is to provide insight and transparency for the association. It should be used to highlight to the membership base, the Board, and other users of the financial statements how the association’s funds are used to support programs and cover overhead costs.

Nonprofit watchdog agencies have long supported the idea that a nonprofit should have a high percentage of its expenses allocated to the program service functions. However, the actual amount of overhead costs that go into running an association and permit the program services to flourish is typically underestimated. Associations must make investments in their future through improving relationships, processes, and tools (supporting service expenses) that will allow them to continue to provide and grow their program services.

How are Expenses Allocated Across the Functional Areas?

It is expected that some expenses will be allocated 100% to management and general expenses as they benefit the association as a whole. For instance, salaries of positions like the bookkeeper or controller should be allocated fully to management and general unless that individual spends a portion of their time providing program services to members. Costs incurred in outsourcing bookkeeping, or completing an annual audit are considered to benefit the association as a whole and not one program in particular.

Other expenses may be allocated 100% to the program services, like event insurance for the annual conference, or printing costs to produce the quarterly magazine.

Other costs may have elements of both and can be allocated accordingly using a reasonable allocation method. For instance, salaries and related expenses could be allocated based on how an individual employee spends their time on different program services and overhead activities in a typical month. The breakout of salaries could also be translated into the square footage of the leased office space to allocate rent expense. Allocation methods can vary widely from one association to another and from one type of expense to another. It’s important to use reasonable allocation methodologies that are be justified, documented, and applied consistently.

What About 501(c)(3) Associations?

It’s not uncommon for an association to be exempt under 501(c)(3), or for an association to have a related 501(c)(3) organization. When we talk about functional expense reporting, the major difference between a 501(c)(6) and a 501(c)(3) is the fundraising element.

Fundraising, sometimes referred to as development or advancement, is an element of the supporting activities. Fundraising activities involve courting or seeking potential donors to contribute to the organization through donation of funds, in-kind support, or time. These activities can be accomplished through public or private fundraisers, capital campaigns, special events, distribution of mailers, time spent with potential donors, costs of solicitation, or a myriad of other activities.

Examples costs related to fundraising include development staff and executive director salary including benefits, cost of printing and postage for invitations or direct mailings, and the costs of events or outreach activities. If determined through appropriate allocation methods, costs should be allocated to this functional expense category as well.

If your association reports support revenue from contributions or grants, it’s extremely likely you have some fundraising costs that should be reported in the statement of functional expenses. Keep in mind these costs might not be direct costs but could be allocated from salaries of personnel who spend a portion of their time at events or meeting with supporters, or the cost of your website, mailings, and publications where the association solicits support.

What now?

As your association closes out the next reporting period and starts to prepare financial statements, keep in mind the key requirements of functional expense reporting and consider how you’ve presented your expenses. Could you improve your presentation? Are there additional expenses that should be reallocated?

Consider how your association tracks expenses within the accounting system. Could improvements be made to make functional expense reporting easier or more accurate? Changes like utilizing classes or additional account codes could help track expenses in functional categories throughout the year to make year-end reporting easier.

Have you documented the allocation methodologies used in the association? Perhaps you’re using an outdated employee time study to allocate certain costs. It may be time to refresh the study and make changes to the allocations.